When you agree to marry someone legally, you merge your entire life with your partner. So be it your personal issues or finances, everything needs sharing to move forward together. Financial intimacy is crucial and needs utmost attention as you embark on this journey. As a newly married couple, with proper financial planning, you can avoid future conflicts and build a strong financial foundation together.

So be it your personal issues or finances, everything needs sharing to move forward together.

Financial intimacy is crucial and needs utmost attention as you embark on this journey.

You need not be on the same page with your partner regarding every financial decision.

However, you must work in unison by communicating and finding a middle ground wherever necessary.

Money can be a sensitive topic that invites arguments. Therefore, newlyweds must talk about it as soon as possible to begin on the right foot.

Let this blog be an enlightening guide to help you discuss your financial planning and goals with your partner without hassle.

Discuss your views on money

Every person has a different childhood that impacts their views and thoughts about money.

It influences their money saving, spending, and investing habits.

Therefore, dive into the money conversation by touching upon childhood.

Understand each other’s experiences of having no, little, or too much money at different points and how it shaped your opinions.

A thorough and intimate discussion about your childhood financial state and current money habits will steer you in the right money management direction.

Find financial goals and priorities

Once you know your partner’s existing money skills, discuss the prospects.

Ask each other about your individual goals and collective family goals.

You can achieve a balance between the two by conversing about expenses, income, accounts, and related topics honestly with your partner.

When discussing financial goals and priorities as a family, it would be wise to form a periodic budget.

Working towards the commonly shared goals like the following would require planning and contribution from both ends.

Buying a home

Most married couples decide to purchase their own home or apartments post-wedding.

This decision is the most considerable financial investment choice.

Therefore, careful and detailed planning is necessary to save, invest, and leverage debt to buy a home while growing wealth.

Debt leveraging

Many people consider living debt-free as the greatest asset they could own.

Similarly, others choose to keep a specific debt level in the mix for particular benefits like growth.

Discuss with each other your thoughts regarding keeping debt or finishing it.

Children conversations

Having a child does not just take a toll on an individual’s physical and emotional well-being but also affects the finances considerably.

Therefore, it is critical to converse about having a kid and determining a contribution pattern for its savings beforehand.

Career changing decisions

While every person has the right to switch careers whenever they like, it is critical for newlyweds to discuss it early. This decision impacts their and the family’s life.

Therefore, make choices about financial handling until the other person gets a job, advances in their studies, etc.

Investing in other’s hobbies

Each individual has unique hobbies. While some require no investment, others require hefty sums of money.

For instance, collecting stamps, coins, bottle caps, etc., may not require considerable money. But sports, foreign vacations, wine collections, etc., are expensive hobbies.

Therefore, creating a monthly or periodic budget to save for such pursuits is advisable.

It assists in not only money saving but also strengthens your bond as you care for each other’s interests.

Retirement planning

While some can’t wait to get rid of their 9-5 jobs by retiring early, others may continue the hustle until the end to build the envisaged empire.

Therefore, retirement decisions may vary according to the couple’s mental, physical, and emotional choices.

To retire early, you must start saving and investing continuously. You must address the benefits of compound interest and begin saving.

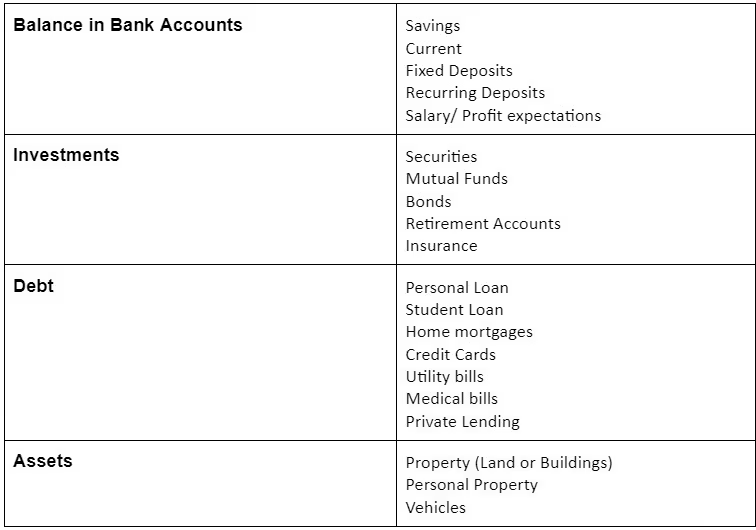

Discussions around the current financial structure

You can build a robust financial future by taking the first step of discussing your current position.

As partners, you must strengthen your trust by being open and honest.

If any of you withhold information, lie, etc., for fear or embarrassment, it will cause significant problems in the future.

Your current financial reality discussions can revolve around the following resources and obligations:

Plan finances and budgets

Budgeting is a crucial step in money management and can become overwhelming.

However, limiting spending and saving for your goals can be fun if you know how to manage your colliding thoughts.

When you have visibility into your financial conditions, you can start planning toward your future goals.

Sticking to a budget can help you keep each other in line and support you through the process.

The spending habits improve as you define the saving areas and lower expenses accordingly.

You can have this conversation at least once a year and stick through it.

Furthermore, you must track your progress and not forget the plan.

Usually, when we get caught up in the routine after marriage, we may indulge in miscellaneous spending without care.

On the other hand, it is also possible to keep as little of a spendable amount and live in misery.

A healthy balance is necessary to keep the fun and know you are in the right financial direction per your plan.

Giving back to the community

While using your money for your goals and likings is crucial, giving back to the community should also be a consideration in your financial planning.

Generosity can be through donations, volunteering, or expanding your skills for a cause.

In any case, communicate with your partner how you would like to serve your environment.

Discover ways through which you can share your talents and finances for a specific cause that doesn’t concern you but others.

Estate planning

Estate planning doesn’t sound like a decision newlyweds should consider so early.

However, with time uncertainties, these discussions allow you to safeguard the other person after one of you dies.

It is, in a true sense, a form of caring for your partner from the after-world.

Estate planning becomes critical when you have kids or separate assets. The crucial documents in this stage are-

A binding will and testament

Instead of the courts making significant decisions for you and your assets, the last will and testament enable you and your partner to do so.

You can make decisions regarding inheritance, children’s guardians, etc.

Moreover, you can write about what will happen to your asset after you leave for the netherworld.

The idea is to protect your assets from courts and ensure everything goes where you like.

Getting the courts involved can be messy as they may not do what you want. A legal document is far better than a handwritten will and must get submitted on time.

A current living will

Discussions about the living will help you kickstart conversations around complex end-of-life events.

It is not pulling the plug, but a form of care and love by telling them your wishes without hassle and guessing.

Power of attorney

If you’re incapacitated or cannot handle finances yourself, a power of attorney is to whom you give this responsibility for the time.

The individual should delegate the financial affairs to a trusted person to keep them in order.

Healthcare power of attorney

When the medical authorities declare you incapacitated, a healthcare power of attorney empowers a person you trust to manage your finances.

In other words, it shows whom you trust the most for crucial decisions.

Combining finances- yay or nay?

One critical decision newlyweds have to consider is whether they should keep their finances separate or combine them.

These decisions can get influenced by family history or other life-changing events.

For instance, if you’ve seen betrayal among your family or friends, you might lean towards keeping them distinct.

However, if your parents kept the money combined, you may get prompted to do the same.

In both cases, several benefits and challenges remain. These include

Merits to combining finances

Strengthens trust

When you decide to combine finances with your partner, it builds transparency and trust with each other.

Simplified budgeting

The budgeting process is simplified as you manage your money together, not separately.

Unity

Combining finances binds your union stronger and encourages robust unity.

Drawbacks to combining finances

Feeling of being dependant

Combining finances can be highly challenging if you have been independent with your money choices.

You might feel dependent on your partner to decide whether you should purchase or invest in something.

However, there’s a way you can work around this situation, which requires you to be open and accountable.

Guilt-like feeling

Another limitation of combining finances is the feeling of guilt for spending.

You might have discussed spending limits with your partner, but the occasional sale drew you closer.

This feeling can cause resentment among the newlyweds. You must consider the thin line in front of you and manage your financial affairs accordingly.

Debt differences

If one of you has significant debt while the other has none, combining finances would seem to be a burden.

However, if your bond is strong, these disparities will not affect you.

Bottom line

As newlyweds, you assume new roles and responsibilities in your and your partner’s lives. Financial planning is one aspect where actionable steps and comfort today will eliminate future worries. Therefore, find your financial happily ever after by considering the points mentioned in the blog and being transparent with each other.