The Unified Payments Interface (UPI) has revolutionized how we manage money completely. Do you remember when you had to scramble for stray coins or wait days for a bank transfer to go through? Those days are over.

You may now pay for groceries, a chai from a roadside stand, or supper with friends with only a quick scan and a PIN entry. It's quick, easy, and available everywhere.

But here's the other side: scammers chase money wherever it goes.

We enjoy how easy digital payments are, but there is a rising dark side to this technology: phony UPI payments. You may have already run into something that felt "off" if you operate a store, work for yourself, or use UPI every day.

You might have seen a screen that said "Payment Successful," but your phone never buzzed. You might have gotten a message that looked like a bank alert but felt different.

We will talk about how these things happen, the methods that scammers use (such as phony payment screenshots and fake UPI payment apps), and most importantly, how to keep your hard-earned money safe.

What Exactly Is a Fake UPI Payment?

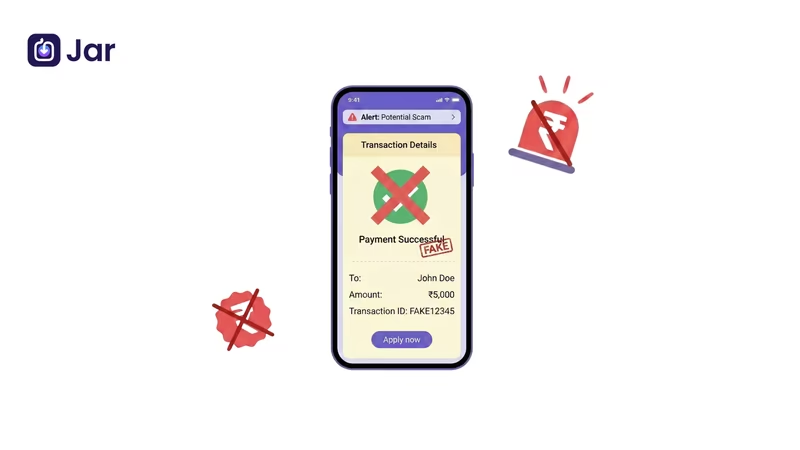

Before we get into the hard stuff, let's make sure we know what we're talking about. A phony UPI payment is exactly what it sounds like: a scammer makes you think they sent money to your bank account when they really didn't send a single rupee.

It's like getting a photocopy of a dollar bill instead of the actual thing. It might look like money to someone who isn't paying attention or is in a hurry. But it doesn't have any value.

Scammers use a variety of tools to pull this off. They might use photo-editing software to doctor a screenshot, or worse, they might use malicious apps designed specifically to mimic the interface of popular payment apps like Google Pay, PhonePe, or Paytm. The goal is simple: to get you to hand over goods, services, or even cash, based on a lie.

Jar is an app that automatically detects your spare change from daily UPI transactions and invests it into 24K Digital Gold. Download Jar now.

How Do Fake UPI Scams Work?

| Feature | Genuine Transaction | Fake/Spoof Screenshot |

| App Notification | Instant push notification from your UPI app. | No notification appears on your device. |

| Bank SMS | Official SMS from your bank (e.g., AD-HDFCBK). | No SMS, or a fake SMS from a regular 10-digit number. |

| Transaction ID | 12-digit UTR number that is searchable in your history. | Missing, blurred, or random numbers. |

| Wallet Balance | Reflects immediately in your "Transaction History." | Balance remains unchanged. |

| Visual Quality | Crisp text and official branding. | Blurry logos, mismatched fonts, or old timestamps. |

Common Types of Fake UPI Payment Scams

You might be wondering, "How can someone fake a digital transaction? Isn't it all tracked?" Well, yes, real transactions are tracked. But scammers thrive on the gap between human trust and digital verification.

Here are the most common methods they use to execute a fake UPI payment:

1. The "Fake Payment Screenshot" Trick

This is perhaps the oldest trick in the book, yet it remains surprisingly effective. Here is the scenario: You are running a busy shop. A customer buys items worth ₹2,000.

They pull out their phone, pretend to scan your QR code, and then flash their screen at you. You see the familiar green tick, the words "Transaction Successful," and the correct amount. You let them go.

Later, you check your bank balance and realize the money never came. What happened? The customer didn't make a payment.

They simply showed you an old screenshot from a previous transaction, or they used a photo editor to change the date, time, and amount on an old receipt. In the rush of business, you trusted your eyes instead of your bank account.

2. Fake UPI Payment Apps (The "Spoof" Apps)

This is a more dangerous evolution of the screenshot scam. Developers with malicious intent have created fake UPI payment apps that look and behave almost exactly like the real ones.

These apps allow the scammer to enter any name, any amount, and any transaction ID. When they hit "Pay," the app generates a "Payment Successful" screen that looks 100% authentic, complete with sound effects and animations.

To a shopkeeper or individual glancing at the scammer's phone, it looks like a legitimate transaction. But the app is just a simulation; it’s not connected to the banking network at all.

3. The "Send Money to Receive Money" Scam

This is a classic social engineering tactic. You might put up an ad to sell old furniture online. A "buyer" contacts you and says, "I will pay you via UPI. I am sending a request, just accept it."

You get a pop-up on your phone. It asks for your UPI PIN. The buyer claims, "You need to enter your PIN to receive the money." The Truth: You never need to enter your PIN to receive money on UPI.

You only use your PIN to send money. If you enter your PIN, you are authorizing a payment from your account to theirs.

4. The "Emergency" Hustle

Scammers know that if you have time to think, you’ll catch them. So, they create panic.

They might pretend to be in a rush, saying, "My hospital bill is due, please send the goods immediately, the server is slow so the SMS will come later!" They rely on your empathy and the pressure of the moment to make you skip your verification process.

See the full list of countries that accept UPI payments

The Risks: It’s More Than Just Losing Cash

When we talk about fake UPI payments, the immediate thought is financial loss. And yes, that is the biggest hit.

But for businesses, especially small and medium enterprises (SMEs), the risks go deeper.

Financial Drain

For a small shopkeeper, losing even ₹500 or ₹1,000 a few times a week adds up. It eats into your margins.

If you are selling high-value items like electronics or jewelry, a single fake payment can wipe out a month's profit.

Operational Chaos

Imagine you realize a payment was fake after the customer has left. Now you have to spend hours checking your bank statements, calling your bank, and trying to trace the transaction. This wastes valuable time that you should be spending on running your business.

Trust Issues and Reputation Damage

This is a silent killer. If your staff becomes paranoid about every customer because of recent scams, they might start treating genuine customers with suspicion. This friction can ruin the customer experience.

On the flip side, if you are known as a shop that’s "easy to trick," you might become a target for more scammers.

Confused between UPI-linked cards and wallet payments? Read the full comparison.

Common Types of UPI Fraud You Must Know

To be an effective "SEO analyst" of your own finances, you need to know the keywords of fraud. Here are the specific variations of scams you might encounter:

Phishing Links

You receive an SMS or WhatsApp message: "Congratulations! You have won ₹5,000 cashback! Click this link to claim." Clicking the link takes you to a fake website that looks like your bank’s login page.

You enter your UPI ID and PIN, thinking you are logging in. In reality, you just handed your keys to the thief.

Money Muling

This is a sophisticated crime. Scammers might ask you to receive a payment on their behalf and transfer it to another account, promising you a small "commission." By doing this, you become a "money mule."

You are effectively laundering stolen money. When the police track the stolen funds, the trail ends at your bank account, not the scammer's. You could face legal trouble for aiding a crime you didn't know you were committing.

SIM Swap Fraud

Your phone suddenly loses network signal. You think it's a glitch. In reality, a scammer has convinced your mobile operator to issue a new SIM card for your number (pretending to be you).

Once they have the new SIM, they have access to all your OTPs. They can reset your UPI PINs and drain your accounts before you even realize your phone is dead.

Fake Rewards and "Collect Request" Scams

This involves the "Collect Request" feature of UPI. Scammers send a payment request disguised as a refund or a cashback offer.

The message might say "Refund of ₹200 credited," but the button says "Pay." If you are not paying attention, you click "Pay," enter your PIN, and the money leaves your account instead of entering it.

Learn what a UTR number is and how to track your payments easily.

How to Identify a Fake UPI Payment

Now, let’s get to the most critical part of this guide. How do you spot a fake? You don't need to be a tech genius; you just need to be observant.

1. No SMS or Bank Notification

This is the golden rule. If your phone didn't buzz, the money isn't there. Scammers will say, "The server is down," or "The bank is slow today." Do not believe it. Always wait for the confirmation message from your bank or your UPI app. Do not rely on the SMS shown on their phone; fake SMS apps exist too!

2. The "Payment Successful" Screen Looks Weird

If you look closely at fake payment screenshots, you’ll often find errors:

- Font Mismatch: The font used for the amount might look slightly different from the rest of the text.

- Blurry Logos: The bank logos might look pixelated or stretched.

- Wrong Date/Time: The timestamp might be from yesterday, or the time might not match the current time on your clock.

- Missing Transaction ID: A real UPI transaction always has a unique 12-digit UTR (Unique Transaction Reference) number. Fake apps often generate random numbers or leave this blank.

3. Mismatched UPI ID

Check the sender's UPI ID. Legitimate IDs usually follow a pattern (like name@bankname). Scammers often use confusing or random strings of characters, or they might use a handle that looks official but has a typo (e.g., sbi.support@oksbi instead of a verified merchant ID).

4. Urgency and Aggression

A genuine customer will understand if you want to verify the payment. A scammer will get impatient. If someone starts saying, "Hurry up, I have to go," or "Why don't you trust me?" take a step back. This pressure is a tactic to stop you from checking your phone.

5. The Magic "Balance Check"

Sometimes scammers will say, "I sent the money, check your balance." If you don't see the credit, they might ask you to scan a QR code to "force the server to update." Never do this. Scanning a QR code will never help you receive money; it will only help them take it.

Read the full guide on GST charges and limits on UPI payments.

What to Do If You’ve Been Scammed?

It’s a sinking feeling when you realize you’ve been tricked. But you need to act fast.

- Contact Your Bank Immediately: Call your bank’s official customer care number (find it on their website, not on Google Search, as scammers post fake helpline numbers too!). Ask them to freeze your account or block your UPI ID.

- Report to the National Cyber Crime Portal: In India, you can dial 1930 to report online financial fraud. You can also file a complaint at [suspicious link removed].

- Report on the App: Go to the "Help & Support" section of the UPI app (GPay, Paytm, etc.) and report the specific transaction as fraudulent.

- Lodge an FIR: For significant amounts, visit your nearest police station and file an FIR. Provide screenshots, the scammer’s phone number, and transaction details.

Want to know which UPI apps dominate in 2026? Read the full guide.

Technical Solutions for Merchants (Soundboxes)

Beyond the Screen: Best Tools for Merchant Safety If you run a business, relying on your phone screen isn't enough. Consider these tools:

- UPI Soundboxes: Devices from Paytm, PhonePe, or BharatPe that announce "Payment of ₹500 received" out loud. This eliminates the need to look at the customer's phone.

- Merchant-Specific Apps: Use the "Business" version of UPI apps (like GPay Business) which provide real-time dashboards that are harder to spoof than personal accounts.

- Static vs. Dynamic QR Codes: Use dynamic QR codes generated on a POS machine for high-value transactions, as these are much harder to fake.

Direct Comparison: Spotting "Spoof Apps"

Specific Red Flags in Fake UPI Apps:

- Font Mismatch: Look closely at the "Amount" field. In spoof apps, the font of the number often looks slightly thicker or thinner than the text around it.

- Non-Clickable Buttons: In a real app, you can click on the transaction to see "Debited from" or "Check Balance." In a fake screenshot, the image is static.

Missing UTR: Every real UPI transaction has a 12-digit Unique Transaction Reference (UTR). If this is missing or looks like "123456789012," it is 100% fake.

Don't let the rise of fraudulent UPI payment scams keep you from using digital payments. UPI is a great tool that helps us run our businesses more smoothly. The most important thing is to utilize it with your eyes wide open.

Your phone is like your digital wallet. You wouldn't give your real wallet to a stranger, would you? Don't let a stranger's screen tell you how much money you have, either.

You can protect yourself against scams by solely believing your bank warnings, employing soundboxes, and knowing the difference between "sending" and "receiving."

Keep in mind that care is the most important thing when it comes to digital payments. Stay secure, check every transaction, and make sure your hard-earned money stays in your account.

Frequently Asked Questions (FAQs)

Is there a fake UPI app?

Yes, there are numerous "spoof" or "prank" applications designed to mimic the user interface of popular UPI platforms like Paytm, Google Pay, and PhonePe. These malicious apps allow fraudsters to manually enter a recipient's name, a specific amount, and a fake transaction ID to generate a realistic-looking "Payment Successful" screen.

These screens often include authentic-looking animations, brand logos, and even simulated voice confirmation sounds to deceive merchants into believing a transaction has occurred.

Because these apps are not connected to actual banking servers, no money is ever moved, making it critical for users to verify payments via their own bank SMS or transaction history rather than trusting the sender's device.

Can a fake UPI payment be reversed?

Technically, a fake UPI payment cannot be "reversed" because no actual transfer of funds ever took place; the transaction was merely a visual fabrication on a spoof app.

However, if you have been a victim of a real fraudulent transaction, such as being tricked into sending money via a "Collect Request," you can initiate a reversal process by acting immediately.

You should report the transaction to your bank and the NPCI portal within 24 to 48 hours to increase the chances of a successful recovery. While banks cannot unilaterally pull money back once it has reached the scammer's account, they can coordinate with the recipient's bank to freeze the funds if the fraud is reported before the scammer withdraws the cash.

Can I create my own UPI ID?

Yes, you have the flexibility to create and customize your own UPI ID, also known as a Virtual Payment Address (VPA), through any UPI-enabled application.

While the "handle" or suffix (like @oksbi or @paytm) is determined by the app and its partner bank, you can often choose the initial part of the ID, provided it is not already taken by another user.

Most apps like Google Pay and PhonePe allow you to manage multiple UPI IDs for a single bank account, which can help improve transaction success rates by routing payments through different servers.

To do this, simply navigate to the "Payment Settings" or "Bank Account" section of your app and select the option to "Add" or "Edit" your UPI IDs.

How to report a fake UPI transaction?

Reporting a fake or fraudulent UPI transaction requires a multi-step approach to ensure both legal and financial action is taken. First, you should use the "Report" or "Help" feature within your specific UPI app (like GPay or Paytm) to flag the transaction ID.

Simultaneously, you must call the National Cyber Crime Helpline at 1930 or file a formal complaint at the official government portal, cybercrime.gov.in.

Additionally, you should notify your bank's fraud department immediately to freeze your account if you suspect your credentials have been compromised.

For unresolved issues, you can escalate the matter to the NPCI’s Dispute Redressal Mechanism on their official website or eventually to the RBI Ombudsman.

How to identify a fake UPI payment?

Identifying a fake UPI payment requires looking past the "Success" screen and verifying the transaction through official channels.

The most reliable method is to wait for the official SMS notification from your bank or to manually check your own app's transaction history to confirm the balance has actually increased.

Visually, fake screenshots often contain subtle red flags such as mismatched fonts (where the amount looks different from the surrounding text), incorrect timestamps that don't match the current time, or a missing 12-digit UTR (Unique Transaction Reference) number.

Furthermore, always remember that receiving money via UPI never requires you to enter your PIN or scan a QR code; if a sender asks you to do either, it is a guaranteed scam attempt.